|

| 1 | |

Which of the following is true about a flexible budget? |

| | A) | It is based on one level of activity. |

| | B) | It treats fixed costs as if they are variable costs. |

| | C) | It is based on an unlimited range of activity. |

| | D) | It provides a means of comparison between actual and expected costs at the actual level of activity. |

|

|

|

| 2 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_02.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (8.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_02.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (8.0K)</a>

At an actual level of 6,200 process hours, what will be the expected utilities expense if you use the concepts of a flexible budget? |

| | A) | $22,500 |

| | B) | $18,750 |

| | C) | $18,600 |

| | D) | $26,250 |

|

|

|

| 3 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_03.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (17.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_03.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (17.0K)</a>

What are the expected costs at an activity level of 7,000 process hours, if you use the concepts of a flexible budget? |

| | A) | $31,500 |

| | B) | $33,250 |

| | C) | $34,300 |

| | D) | $31,033 |

|

|

|

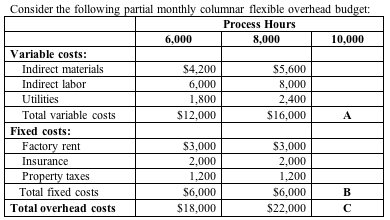

| 4 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_04.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (31.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_04.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (31.0K)</a>

What are the values of A, B, and C, respectively, at 10,000 process hours? |

| | A) | A= $20,000; B = $10,000; C = $30,000 |

| | B) | A = $20,000; B = $6,000; C = $26,000 |

| | C) | A = $14,000; B = $6,000; C = $20,000 |

| | D) | A = $18,000; B = $6,000; C = $24,000 |

|

|

|

| 5 | |

Which of the following is the formula flexible budget? |

| | A) | (Budgeted variable-overhead cost per activity unit x Total activity units) + Budgeted fixed overhead cost for the month |

| | B) | (Budgeted variable-overhead cost per planned-activity unit x Total activity units) + Budgeted fixed overhead cost for the month |

| | C) | (Actual variable-overhead cost per activity unit x Total activity units) + Budgeted fixed overhead cost for the month |

| | D) | Budgeted variable and fixed cost per unit x Total planned process hours |

|

|

|

| 6 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_06.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_06.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a>

Based on the columnar flexible budget above, what is the formula flexible budget for 7,500 process hours? |

| | A) | Total monthly overhead costs for 7,500 process hours = ($3.00 x 7,500) + $10,000 |

| | B) | Total monthly overhead costs for 7,500 process hours = ($3.00 x 7,500) + $7,500 |

| | C) | Total monthly overhead costs for 7,500 process hours = ($3.30 x 7,500) + $10,000 |

| | D) | Total monthly overhead costs for 7,500 process hours = ($3.30 x 7,500) + $12,500 |

|

|

|

| 7 | |

A major difference between normal costing and standard costing systems is which of the following? |

| | A) | Under standard costing, overhead is applied at actual hours |

| | B) | Under normal costing, overhead is applied at actual hours |

| | C) | Under standard costing, overhead is applied at standard hours allowed |

| | D) | Both (B) and (C) |

|

|

|

| 8 | |

Which of the following has traditionally been the most popular activity measure in manufacturing firms? |

| | A) | Direct-labor time |

| | B) | Machine hours |

| | C) | Process time |

| | D) | Direct materials |

|

|

|

| 9 | |

Which of the following is not a criterion for choosing an activity measure? |

| | A) | Identifying the cost driver that most significantly affects overhead costs |

| | B) | The activity measure and the variable-overhead costs move together as overall productive activity changes |

| | C) | The activity measure must be a dollar measure |

| | D) | Using an activity measure that is more closely linked with changing manufacturing technology |

|

|

|

| 10 | |

Budgeted variable overhead for the level of production achieved is 40,000 machine-hours at a budgeted cost of $62,000. Actual variable overhead at the level of production achieved was 38,000 hours at an actual cost of $62,400. What is the total variable overhead variance? |

| | A) | $400 favorable |

| | B) | $400 unfavorable |

| | C) | $3,100 unfavorable |

| | D) | $3,100 favorable |

|

|

|

| 11 | |

Actual variable overhead is $24,600 and budgeted variable overhead at 10,000 machine-hours is $24,000. What is the variable-overhead spending variance? |

| | A) | $500 |

| | B) | $600 |

| | C) | $100 |

| | D) | Cannot be determined from the information provided. |

|

|

|

| 12 | |

The variable-overhead spending variance is $1,080, unfavorable. Variable overhead budgeted at 40,000 process hours is $50,000. Actual process hours were 36,000. What was the actual variable-overhead rate per process hour? |

| | A) | $1.28 |

| | B) | $1.25 |

| | C) | $1.39 |

| | D) | $1.52 |

|

|

|

| 13 | |

Actual variable overhead at 29,000 process hours is $22,600. Budgeted variable overhead at 30,000 process hours is $24,000. What is the variable-overhead efficiency variance? |

| | A) | $ 20 unfavorable |

| | B) | $600 favorable |

| | C) | $600 unfavorable |

| | D) | $800 favorable |

|

|

|

| 14 | |

Actual variable overhead is $25,800. Budgeted variable overhead at 25,000 process hours is $25,000. The variable-overhead efficiency variance is $800, favorable. How many process hours were actually used? |

| | A) | 25,000 |

| | B) | 24,800 |

| | C) | 24,200 |

| | D) | 24,400 |

|

|

|

| 15 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_15.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (22.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_15.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (22.0K)</a>

Which of the following is true? |

| | A) | The difference between A and B is a favorable variable-overhead spending variance. |

| | B) | The difference between A and B is an unfavorable variable-overhead spending variance. |

| | C) | The difference between B and C is a favorable variable-overhead efficiency variance. |

| | D) | The difference between A and B is a favorable variable-overhead efficiency variance. |

|

|

|

| 16 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_16.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (23.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_16.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (23.0K)</a>

Which of the following is true? |

| | A) | The difference between A and B is a favorable variable-overhead spending variance. |

| | B) | The difference between B and C is an unfavorable variable-overhead efficiency variance. |

| | C) | The difference between B and C is a favorable variable-overhead efficiency variance. |

| | D) | The difference between A and B is a favorable variable-overhead efficiency variance |

|

|

|

| 17 | |

Which of the following statements is true about the variable-overhead spending variance? |

| | A) | An unfavorable variance means that the total actual cost of variable overhead is greater than expected, after adjusting for the actual quantity of process hours used. |

| | B) | An unfavorable variance could result from paying a higher-than-expected price per unit for variable-overhead items. |

| | C) | An unfavorable variance could result from using more of the variable-overhead items than expected. |

| | D) | All of the above are true about the variable-overhead spending variance. |

|

|

|

| 18 | |

Budgeted fixed overhead is $45,000. Actual fixed overhead was $42,000. What is the fixed-overhead budget variance? |

| | A) | $3,000 unfavorable |

| | B) | $3,000 favorable |

| | C) | $8,000 unfavorable |

| | D) | $8,000 favorable |

|

|

|

| 19 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_19.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (11.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_19.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (11.0K)</a>

Using the variable designations given above, determine which of the following expresses the fixed-overhead volume variance? |

| | A) | Actual Fixed Overhead - Budgeted Fixed Overhead |

| | B) | SVR(AH - SH) |

| | C) | (PFR x Planned Activity) - (PFR x SH) |

| | D) | AH(PFR - SVR) |

|

|

|

| 20 | |

Budgeted fixed overhead is $36,000 for a planned capacity of 18,000 process hours. The fixed-overhead volume variance was $2,400 unfavorable. What were the standard hours allowed for the number of units produced? |

| | A) | 19,200 |

| | B) | 16,800 |

| | C) | 18,000 |

| | D) | 18,600 |

|

|

|

| 21 | |

You have leased a 5,000-gallon storage tank for $5,000 per month. You stored 4,000 gallons of liquid in the tank during the month. The cost of storage was $1.25 per gallon (= $5,000/4,000) rather than $1.00 per gallon based on 5,000 gallon capacity. Therefore, the cost of storing 4,000 gallons was $1,000 more ($.25 x 4,000) in total than if you had stored 5,000 gallons of liquid in the tank. The $1,000 can be described as which variance? |

| | A) | Variable-overhead efficiency variance |

| | B) | Fixed-overhead spending variance |

| | C) | Variable-overhead spending variance |

| | D) | Fixed-overhead volume variance |

|

|

|

| 22 | |

In an overhead cost performance report, which variance is not reported? |

| | A) | Variable-overhead spending variance |

| | B) | Variable-overhead efficiency variance |

| | C) | Flexible budget for standard process hours |

| | D) | Fixed-overhead volume variance |

|

|

|

| 23 | |

Which of the following is true about an activity-based flexible budget? |

| | A) | It is based on cost drivers assigned to various cost pools. |

| | B) | It is a less accurate reporting device than the traditional flexible budget. |

| | C) | It treats facility level costs as fixed costs. |

| | D) | uses both (A) and (C). |

|

|

|

| 24 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_24.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (43.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_24.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (43.0K)</a>

The manufacturing activity in November consisted of 8,000 process hours, 100 production runs, 800 products tested, and 16,000 direct materials handled. What is the activity-based flexible budget for November? |

| | A) | $37,300 |

| | B) | $36,100 |

| | C) | $30,700 |

| | D) | $41,450 |

|

|

|

| 25 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_25.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (43.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0070667705/388289/ch11_25.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (43.0K)</a>

The limousine rental activity for the year consisted of 50,000 miles and 300 customer contacts. What is the activity-based flexible budget for the year? |

| | A) | $84,600 |

| | B) | $30,700 |

| | C) | $77,100 |

| | D) | $74,700 |

|

|