|

| 1 | |

The economic profits of firms in long-run competitive equilibrium are: |

| | A) | negative. |

| | B) | positive. |

| | C) | zero. |

| | D) | zero if it is a constant cost industry, positive otherwise. |

|

|

|

| 2 | |

Which of the following is a characteristic of equilibrium in long-run competitive markets? |

| | A) | Consumer surplus is minimized |

| | B) | Producer surplus exceeds consumer surplus |

| | C) | Combined consumer and producer surplus is maximized |

| | D) | The difference between producer surplus and consumer surplus is maximized |

|

|

|

| 3 | |

The long-run industry supply curve will be horizontal: |

| | A) | in a decreasing cost industry. |

| | B) | if resource prices rise at the same rate as industry demand rises. |

| | C) | if resource prices fall at the same rate as industry demand rises. |

| | D) | if resource prices remain constant as industry demand rises or falls. |

|

|

|

| 4 | |

Allocative efficiency in the production of wheat requires: |

| | A) | producing every unit of wheat whose marginal benefit equals or exceeds its marginal cost. |

| | B) | that each wheat farm produces its output at minimum average variable cost. |

| | C) | zero economic profits for all wheat farmers. |

| | D) | maximizing consumer surplus while minimizing producer surplus. |

|

|

|

| 5 | |

"Creative destruction" refers to: |

| | A) | the exit of firms following a long term reduction in demand. |

| | B) | the process by which old industries or technologies are replaced by newer ones. |

| | C) | the unwillingness of competitive firms to adopt new technologies because competition precludes their ability to earn long-run economic profits. |

| | D) | the process by which competitive industries become monopolies in the long run. |

|

|

|

| 6 | |

Suppose a decrease in product demand occurs in a decreasing-cost industry. Compared to the original equilibrium the new long-run competitive equilibrium will entail: |

| | A) | a higher price and a higher total output. |

| | B) | a lower price and a lower total output. |

| | C) | a higher price and a lower total output. |

| | D) | a lower price and a higher total output. |

|

|

|

| 7 | |

Combined consumer and producer surplus is maximized in a competitive market: |

| | A) | at the quantity corresponding to the intersection of the market supply and demand curves. |

| | B) | if the market price exceeds minimum average total cost. |

| | C) | at any output level at least as large as the market equilibrium quantity. |

| | D) | provided price exceeds marginal cost. |

|

|

|

| 8 | |

An increasing cost industry is characterized by: |

| | A) | an upsloping long-run supply curve. |

| | B) | an upsloping long-run demand curve. |

| | C) | a perfectly elastic long-run supply curve. |

| | D) | less than optimal long-run output. |

|

|

|

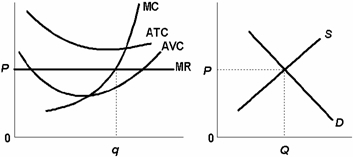

| 9 | |

Use the following diagrams to answer the next question.

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073511447/883736/ch09_q9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (15.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073511447/883736/ch09_q9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (15.0K)</a>

Refer to the above diagrams, which pertain to a purely competitive firm and the industry in which it operates. In the long run we should expect: |

| | A) | new firms to enter, market demand to rise, and price to fall. |

| | B) | demand to increase, and price to rise. |

| | C) | input prices to fall, supply to increase, and price to fall |

| | D) | some firms to exit, supply to decrease, and price to rise. |

|

|

|

| 10 | |

In the long run, competitive markets achieve: |

| | A) | allocative efficiency because P = min ATC but not productive efficiency because P > min AVC. |

| | B) | allocative efficiency because P = MC and productive efficiency because P = min ATC. |

| | C) | productive efficiency because P = min ATC but not allocative efficiency because P > MR. |

| | D) | neither productive nor allocative efficiency. |

|

|