Origin of the Idea  <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.1 Origin of the term "Economics" | | <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.2 Utility | | <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.3 Marginal Analysis | | <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.4 "Ceteris Paribus" | | <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.5 Opportunity Cost |

| <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.1 Origin of the term "Economics" |

The term "economy," from which we get "economics," comes most directly from the Old French word "economie," meaning "management of a household." The French adopted the term from the Latin word "oeconomia," which was in turn derived from the Greek word "oikonomia." Oikonomia came from the word "oikonomos," which separates into "oikos," meaning house, and "-nomos" meaning managing. The oldest recognized written work in the field of economics is Oeconomicus, a book on farming and household management, written by the Greek philosopher Xenophon (430?-355? B.C.). Despite the Greek origins of the term, economics was not an important field of study for the ancient Greeks, who, despite occasional references to economic matters, were more interested in philosophy and ethics.

Photograph courtesy of: (c)Corbis #DEU0094; |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073273082/124320/origin01_1.jpg','popWin', 'width=250,height=370,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (104.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073273082/124320/origin01_1.jpg','popWin', 'width=250,height=370,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (104.0K)</a> |

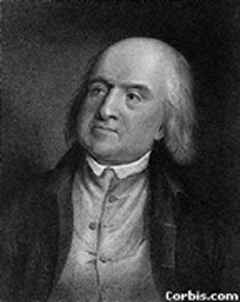

| <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.2 Utility |

The first writings on utility can be traced back to the Englishman Jeremy Bentham (1748-1832). Like many classical economists, Bentham did not begin his academic career studying economics. At age 4 he studied Latin, by age 12 he was enrolled at Queen's College, where he completed his degree at age 15. Bentham then turned to the study of law, but after a short career in the legal profession, devoted his life to the study of philosophy and economics. Bentham held a keen interest in the advancement of scientific knowledge. Prevailing attitudes toward death discourage people of the time from donating their bodies for anatomical research. In an effort to change this, Bentham had his body dissected. That, however, was not the end of Jeremy Bentham. He left his entire estate to University College, London, on condition that he be present at all board meetings. Even today Bentham can be found sitting at University College, his skeleton padded and dressed, with a wax head atop his body (his real head, preserved using South American headhunting techniques, is locked safely away in a college vault). Bentham's philosophy is referred to today as "utilitarianism." Derived from the Greek philosophy of Hedonism, the fundamental principle is that people seek to maximize pleasure and minimize pain. As Bentham expressed it in An Introduction to the Principles of Morals and Legislation in 1780: Nature has placed mankind under the governance of two sovereign masters, pain and pleasure. It is for them alone to point out what we ought to do, as well as to determine what we shall do. On the one hand the standard of right and wrong, on the other the chain of causes and effects, are fastened to their throne. They govern us in all we do, in all we say, in all we think: every effort we make to throw off our subjection, will serve but to demonstrate and confirm it. In words a many may pretend to abjure their empire: but in reality he will remain subject to it all the while.(1)

For Bentham, utilitarianism was not merely an explanation of cause and effect in human behavior, it was an ethical standard, a justification for self-interested behavior. As an ethical standard, Bentham argued that governments should pursue that which promotes the greatest happiness for the greatest number of people. In so doing, however, the government should maximize the community's happiness by promoting individual happiness. The community is a fictitious body, composed of the individual persons who are considered as constituting as it were its members. The interest of the community then is, what? -- the sum of the interests of the several members who compose it. It is vain to talk of the interest of the community, without understanding what is the interest of the individual. A thing is said to promote the interest ... of an individual, when it tends to add to the sum total of his pleasures; or, what comes to the same thing, to diminish the sum total of his pains.(2)

|  <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073273082/124320/origin01_2.jpg','popWin', 'width=290,height=372,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (41.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073273082/124320/origin01_2.jpg','popWin', 'width=290,height=372,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (41.0K)</a> |

The premise that people attempt to maximize pleasure (utility) and minimize pain (disutility) is as important to understanding economic behavior today as it was in Bentham's time.

- Jeremy Bentham, An Introduction to the Principles of Morals and Legislation, (New York: Hafner, 1948), p. 1. [Originally published in 1780].

- Jeremy Bentham, An Introduction to the Principles of Morals and Legislation, (New York: Hafner, 1948), p. 2. [Originally published in 1780.]

Photograph courtesy of: (c)Bettman/Corbis;

| <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.3 Marginal Analysis |

Marginal analysis plays a central role in economic theory, and has for many decades. The first formal expressions of marginal thinking appear in the writings of David Ricardo, who referred to the margins of cultivation in agriculture. Ricardo demonstrated that each additional (marginal) unit of an input (such as fertilizer), would add to total output, but at a diminishing rate and not indefinitely. In short, the world's food supply cannot be grown in a flowerpot, a concept formally known as diminishing marginal returns. While formal marginal analysis started with Ricardo and other classical economists, it exploded with the marginalist school of economic thought and economists such as William Stanley Jevons, Carl Menger, Friedrich von Wieser, and Eugen von Bohm-Bawerk. While Ricardo focused on marginal returns in production, these marginalists focused on utility, attempting to explain how the marginal utility of a good related to its quantity, value, and price. Later marginalists, specifically Francis Edgeworth and John Bates Clark, directed their analysis to issues of production and distribution. Edgeworth formalized and offered a tabular representation of diminishing marginal returns. Clark, applying the concept to labor productivity, stated that: The last tool adds less to man's efficiency than do earlier tools. If capital be used in increasing quantity by a fixed working force, it is subject to a law of diminishing productivity …The diminishing productivity of labor, when it is used in connection with a fixed amount of capital, is a universal phenomenon.

Marginal analysis continues to be an integral part of economic theory, and economists are indebted to the many who have contributed to the development and refinement of marginal thinking.

| <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.4 "Ceteris Paribus" |

The Latin phrase "ceteris paribus" and its use in economic commentary are centuries older than the formal discipline of economics. The first recorded use of the phrase in an economic context was in "De Officiis," written by Cicero in 44 B.C. Cicero (106-43 B.C.) wrote that "the proper way to render aid is - if cetera are paria - to bring it to one who needs it most, and not to one whom we expect to be useful for us." In the late 13th century, the Franciscan friar Petrus Olivi (1248-1298) asserted that goods requiring more labor or greater risk to produce would - ceteris paribus - command a higher price. In the "modern" era of economic thought, first use of the term is attributed to Sir William Petty. Petty wrote that If a man can bring to London an ounce of silver out of the earth in Peru, in the same time that he can produce a bushel of corn, then one is the natural price of the other; now if by reason of new and more easie mines a man can get two ounces of silver as easily as formerly he did one, then corn will be as cheap at ten shillings the bushel as it was before at five schillings, ceteris paribus.

Today the concept of ceteris paribus is so ingrained in economic thinking that the assumption is often used without being explicitly stated, much to the chagrin of those teaching introductory economics.

Sources: Erich Kaufer, Journal of Economic Perspectives, Spring 1997, p. 190-191 (Cicero and Olivi quotes); Charles Henry Hull, ed., The Economic Writings of Sir William Petty vol. 1, p. 50-51. Photograph courtesy of: (c)Photodisc #BUO10579; |  <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073273082/124320/origin01_4.jpg','popWin', 'width=330,height=350,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (50.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073273082/124320/origin01_4.jpg','popWin', 'width=330,height=350,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (50.0K)</a> |

| <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0073273082/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 1.5 Opportunity Cost |

Friedrich von Wieser (1851-1926) first articulated the notion of "opportunity cost" (also referred to as the "alternative-cost" concept) in 1914. Wieser, who born and studied in Vienna, Austria, belonged to a group of economists known as the "Austrian Trio," who built on the growing tradition of marginal analysis. Friedrich von Wieser claimed that: "Whenever the business man speaks of incurring costs, he has in mind the quantity of productive means required to achieve a certain end; but the associated idea of a sacrifice which his efforts demand is also aroused. In what does this sacrifice consist? What, for example, is the cost to the producer of devoting certain quantities of iron from his supply to the manufacture of some specific product? The sacrifice consists in the exclusion or limitation of possibilities by which other products might have been turned out, had the material not been devoted to one particular product. Our definition in an earlier connection made clear that cost-productive-means are productive agents which are widely scattered and have manifold uses. As such they promise a profitable yield in many directions. But the realization of one of these necessarily involves a loss of all the others. It is this sacrifice that is predicated in the concept of costs: the costs of production or the quantities of cost-productive-means required for a given product and thus withheld from other uses."(1)

|  <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073273082/124320/origin02_1.jpg','popWin', 'width=250,height=374,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (48.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0073273082/124320/origin02_1.jpg','popWin', 'width=250,height=374,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (48.0K)</a> | |

Friedrich von Wieser did not invent opportunity costs, he merely formalized the concept for us. Every decision involves an assessment of the opportunity costs involved, and most people make that assessment without ever knowing the term or formal concept.

|

- Friedrich von Wieser, Social Economics, trans. A. Ford Hinrichs (New York: Adelphi, 1927), 99-100. [Originally published in 1914.]

Photograph courtesy of: (c)Nance Trueworthy;

|