|

| 1 | |

The essential characteristics of a liability do not include: |

| | A) | The existence of a past causal transaction or event. |

| | B) | Present obligation. |

| | C) | The existence of a legal obligation. |

| | D) | A future sacrifice of economic benefits. |

|

|

|

| 2 | |

Of the following, which usually would not be classified as a current liability? |

| | A) | A nine-month note to be paid with the proceeds from the sale of common stock. |

| | B) | Bonds payable maturing within the coming year. |

| | C) | Estimated warranty liability. |

| | D) | Subscription revenue received in advance. |

|

|

|

| 3 | |

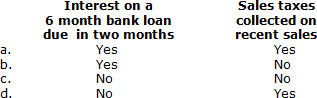

Which of the following results in an accrued liability? <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025834/1061248/Chapter13_q03.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025834/1061248/Chapter13_q03.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a>

|

| | A) | a |

| | B) | b |

| | C) | c |

| | D) | d |

|

|

|

| 4 | |

On November 1, Epic Distributors borrowed $24 million cash to fund an expansion of its facilities. The loan was made by WW BancCorp under a short-term line of credit. Epic issued a 9-month, 12% promissory note. Interest was payable at maturity. Epic's fiscal period is the calendar year. In Epic's adjusting entry for the note on December 31, interest expense will be: |

| | A) | $0 |

| | B) | $240,000 |

| | C) | $480,000 |

| | D) | $640,000 |

|

|

|

| 5 | |

On October 1, 2014, Parton Industries borrowed $12 million cash to provide working capital. The loan was made by Second Bank under a short-term line of credit. Parton issued an 8-month, "noninterest-bearing note." 8% is the bank's stated "discount rate." Parton's fiscal period is the calendar year. In Parton's 2014 income statement interest expense for the note will be: |

| | A) | $0 |

| | B) | $240,000 |

| | C) | $360,000 |

| | D) | $480,000 |

|

|

|

| 6 | |

Commercial paper has become an increasingly popular way for companies to raise funds. Which of the following is not true regarding commercial paper? |

| | A) | Commercial paper is often purchased by other companies as a short-term investment. |

| | B) | Commercial paper usually is sold in minimum denominations of $25,000 with maturities of greater than 270 days. |

| | C) | Interest often is discounted at the issuance of the note. |

| | D) | Usually the interest rate is lower than in a bank loan. |

|

|

|

| 7 | |

On November 1, Shearer Shoes borrowed $18 million cash and issued a 6-month, "noninterest-bearing note." The loan was made by Third Commercial Bank whose stated "discount rate" is 9%. Shearer's effective interest rate on this loan is: |

| | A) | 8.61% |

| | B) | 9.0% |

| | C) | 9.42% |

| | D) | 9.5% |

|

|

|

| 8 | |

Under U.S. GAAP, liabilities payable within one year can be excluded from current liabilities only if: |

| | A) | The business intends to refinance the obligations on a long-term basis. |

| | B) | The business has the demonstrated ability to refinance the obligations on a long-term basis. |

| | C) | Both a and b. |

| | D) | Liabilities payable within one year always must be classified as current liabilities. |

|

|

|

| 9 | |

Under IFRS, a company can demonstrate their ability to refinance long-term debt for purposes of excluding the debt from current liabilities by: |

| | A) | Completing refinancing before the date of issuance of the financial statements. |

| | B) | Completing refinancing before the balance sheet date. |

| | C) | Promising to refinance the liabilities. |

| | D) | None of the above. |

|

|

|

| 10 | |

Reunion BBQ has $4,000,000 of notes payable due on March 11, 2015, which Reunion intends to refinance. On January 5, 2015, Reunion signed a line of credit agreement to borrow up to $3,500,000 cash on a two-year renewable basis. On the December 31, 2014, balance sheet, Reunion should classify: |

| | A) | $500,000 of notes payable as short-term and $3,500,000 as long-term obligations. |

| | B) | $500,000 of notes payable as long-term and $3,500,000 as short-term obligations. |

| | C) | $4,000,000 of notes payable as short-term obligations. |

| | D) | $4,000,000 of notes payable as long-term obligations. |

|

|

|

| 11 | |

Which of the following statements concerning lines of credit is untrue? |

| | A) | A line of credit is an agreement that permits a company to borrow up to a prearranged limit without having to follow formal loan procedures and paperwork. |

| | B) | A noncommitted line of credit is a formal agreement that usually requires the firm to pay a commitment fee to the bank. |

| | C) | Banks sometimes require the company to maintain a compensating balance on deposit with the bank (say 5%) as part of the line of credit agreement. |

| | D) | Most short-term bank loans are arranged under an existing line of credit. |

|

|

|

| 12 | |

On January 1, 2014, Yukon Company agreed to grant its employees two weeks vacation each year, with the provision that vacations earned in a particular year could be taken the following year. For the year ended December 31, 2014, all twelve of Yukon's employees earned $1,200 per week each. Eight of these vacation weeks were not taken during 2014. In Yukon's 2014 income statement, how much expense should be reported for compensated absences? |

| | A) | $0 |

| | B) | $9,600 |

| | C) | $14,400 |

| | D) | $28,800 |

|

|

|

| 13 | |

An enterprise should accrue a liability for compensation of employees' unpaid vacations if certain conditions exist. Each of the following is a condition for accrual except: |

| | A) | Compensation for the vacations is probable. |

| | B) | The employee has the right to carry forward the vacation time beyond the current period. |

| | C) | The amount of compensation is known. |

| | D) | The employee benefit has been earned. |

|

|

|

| 14 | |

In its financial statements, an enterprise should accrue a liability for a loss contingency involving a possible cash payment if certain conditions exist. Each of the following is a condition for accrual except: |

| | A) | The payment is probable. |

| | B) | The cause of the loss contingency occurred prior to the end of the year. |

| | C) | The amount of payment can be estimated before the financial statements are issued. |

| | D) | The obligation is a legally enforceable claim. |

|

|

|

| 15 | |

Which of the following loss contingencies generally do not require accrual? |

| | A) | Manufacturers' product guarantees. |

| | B) | Claims by government agencies with probable negative outcomes. |

| | C) | Obligations due to cash rebate offers. |

| | D) | Retailers' extended warranties. |

|

|

|

| 16 | |

Warren Advertising becomes aware of a lawsuit after the end of the fiscal year, but prior to the issuance of financial statements. A loss should be accrued and a liability should be reported if the amount can be reasonably estimated and: |

| | A) | The cause for action occurred prior to the end of the fiscal year. |

| | B) | The damages would be payable within a year. |

| | C) | Both a. and b. |

| | D) | The contingency should not be accrued. |

|

|

|

| 17 | |

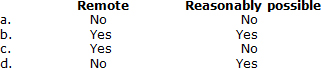

A loss contingency should be accrued when the amount of loss is known and the occurrence of the loss is: <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025834/1061248/Chapter13_q17.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (16.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025834/1061248/Chapter13_q17.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (16.0K)</a>

|

| | A) | a |

| | B) | b |

| | C) | c |

| | D) | d |

|

|

|

| 18 | |

During 2014 Green Thumb Company introduced a new line of garden shears that carry a two-year warranty against defects. Experience indicates that warranty costs should be 2% of net sales in the year of sale and 3% in the year after sale. Net sales and actual warranty expenditures were as follows:

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025834/1061248/Chapter13_q18.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (8.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025834/1061248/Chapter13_q18.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (8.0K)</a>

At December 31, 2015, Green Thumb should report as a warranty liability of: |

| | A) | $900 |

| | B) | $1,250 |

| | C) | $3,750 |

| | D) | $4,500 |

|

|

|

| 19 | |

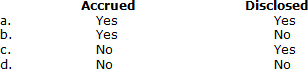

There is a possibility of a safety hazard for a manufactured product. As yet, no claim has been made for damages, though there is a reasonable possibility that a claim will be made. If a claim is made, it is probable that damages will be paid and the amount of the loss can be reasonably estimated. This possible loss must be: <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025834/1061248/Chapter13_q19.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (13.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025834/1061248/Chapter13_q19.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (13.0K)</a>

|

| | A) | a |

| | B) | b |

| | C) | c |

| | D) | d |

|

|

|

| 20 | |

Under IFRS, if every amount in a range of contingent losses is equally likely, the amount accrued is the: |

| | A) | Low end of the range. |

| | B) | High end of the range. |

| | C) | Midpoint of the range. |

| | D) | None of the above. |

|

|

|

| 21 | |

Gain contingencies usually are recognized in the income statement when: |

| | A) | The gain is realized. |

| | B) | The gain is probable and the amount is known. |

| | C) | The gain is probable and the amount can be reasonably estimated. |

| | D) | The gain is reasonably possible and the amount can be reasonably estimated. |

|

|