|

| 1 | |

Which of the following is not one of the activities of the conversion process? |

| | A) | Requisition raw materials |

| | B) | Buy raw material |

| | C) | Use labor and other manufacturing resources to create finished goods. |

| | D) | Store the finished product until sold. |

|

|

|

| 2 | |

The cost of the wages of assembly line supervisor is: |

| | A) | direct labor |

| | B) | indirect labor |

| | C) | manufacturing overhead |

| | D) | selling and administrative |

|

|

|

| 3 | |

The journal entry to record the payment of the assembly line supervisor would include a: |

| | A) | credit to Cost of Goods Manufactured |

| | B) | debit to Work-in-Process Inventory |

| | C) | debit to Manufacturing Overhead |

| | D) | credit to Accounts Payable |

|

|

|

| 4 | |

The journal entry to record the purchase of indirect materials on account would include a: |

| | A) | debit to raw materials inventory |

| | B) | debit to Manufacturing Overhead |

| | C) | debit to Work-in-Process Inventory |

| | D) | credit to Cost of Goods Manufactured |

|

|

|

| 5 | |

The journal entry to record the requisition of raw materials for production would include a: |

| | A) | credit to Direct Labor |

| | B) | credit to Administrative Wages |

| | C) | debit to Manufacturing Overhead |

| | D) | debit to Work-in-Process Inventory |

|

|

|

| 6 | |

The journal entry to record the application of manufacturing overhead to work-in- process inventory is: |

| | A) | debit to Manufacturing Overhead and credit to Work-in-Process Inventory |

| | B) | debit to Work-in-Process and credit to Manufacturing Overhead |

| | C) | debit to Work-in-Process Inventory and credit to Accumulated Depreciation |

| | D) | debit to Cost of Goods Manufactured and credit to Manufacturing Overhead |

|

|

|

| 7 | |

A cost pool is a group of overhead costs that respond to changes in: |

| | A) | a cost driver |

| | B) | conversion costs decreases |

| | C) | conversion costs increases |

| | D) | the level of sales |

|

|

|

| 8 | |

The activity "testing products" is part of the activity level: |

| | A) | product sustaining |

| | B) | facility sustaining |

| | C) | batch related |

| | D) | unit related |

|

|

|

| 9 | |

The activity "handling materials" is part of the activity level: |

| | A) | product sustaining |

| | B) | facility sustaining |

| | C) | batch related |

| | D) | unit related |

|

|

|

| 10 | |

When the amount of over- underapplied manufacturing overhead is large, the Manufacturing Overhead account is generally closed out to: |

| | A) | Cost of Goods Sold |

| | B) | Work-in-Process Inventory |

| | C) | Cost of Goods Manufactured |

| | D) | Finished Goods Inventory, Work-in-Process Inventory, and Cost of Goods Sold |

|

|

|

| 11 | |

Landoll Manufacturing Corporation applies batch-related manufacturing overhead on the basis of the number of production runs. The following information is available:

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078136601/794878/image001.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (7.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078136601/794878/image001.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (7.0K)</a>

The amount of over/underapplied manufacturing overhead is: |

| | A) | $121,405 overapplied |

| | B) | $9,450 underapplied |

| | C) | $0 under/over applied |

| | D) | Cannot Be Determined |

|

|

|

| 12 | |

Price Purification Systems gathered the following direct labor cost information for the month of April:

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078136601/794878/image002.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (12.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078136601/794878/image002.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (12.0K)</a>

The direct labor price variance is: |

| | A) | $47,110 F |

| | B) | $30,643 F |

| | C) | $1,260 U |

| | D) | $45,850 F |

|

|

|

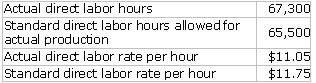

| 13 | |

Price Purification Systems gathered the following direct labor cost information for the month of April:

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078136601/794878/image002.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (12.0K)</a>

The direct labor usage variance is: |

| | A) | $19,890 U |

| | B) | $1,260 F |

| | C) | $2,571 U |

| | D) | $21,150 F |

|

|

|

| 14 | |

Scout & Sons Manufacturing manufactures camping gear. Selected data regarding standard costs and actual results for the month of February are shown below.

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078136601/794878/image003.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (16.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078136601/794878/image003.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (16.0K)</a>

The direct materials price variance is: |

| | A) | $1,650 F |

| | B) | $5,198 F |

| | C) | $5,859 F |

| | D) | $7,560 F |

|

|

|

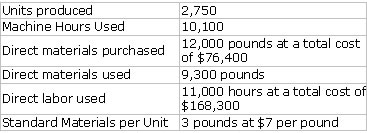

| 15 | |

Scout & Sons Manufacturing manufactures camping gear. Selected data regarding standard costs and actual results for the month of February are shown below.

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078136601/794878/image003.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (16.0K)</a>

The direct materials usage variance is: |

| | A) | $6,689 U |

| | B) | $7,350 U |

| | C) | $661 U |

| | D) | $900 F |

|

|