|

| 1 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_1.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (12.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_1.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (12.0K)</a>

If total overhead is allocated based on machine hours, how much overhead would be allocated to product A? |

| | A) | $1,400,000 |

| | B) | $314,360 |

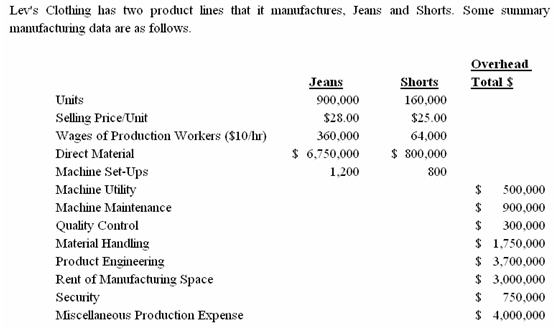

| | C) | $400,000 |

| | D) | $628,710 |

|

|

|

| 2 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_2.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (11.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_2.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (11.0K)</a>

Assume overhead is allocated using ABC, how much overhead would be allocated to product B? |

| | A) | $1,257,440 |

| | B) | $1,173,000 |

| | C) | $733,500 |

| | D) | $628,720 |

|

|

|

| 3 | |

Which of the following best describes the impact of undercosting? |

| | A) | Undercosting all products allows for larger profit margins. |

| | B) | Companies use target pricing to undercost products. |

| | C) | Undercosting some products will lead to overcosting other products, which is an acceptable outcome. |

| | D) | Undercosting some products can lead to overcosting other products which may then become overpriced and lose market share. |

|

|

|

| 4 | |

When establishing an Activity-Based Costing system, an organization's goal is to: |

| | A) | allocate costs to all activities within an organization. |

| | B) | define all activities within the organization and the costs required to perform those activities. |

| | C) | assign costs to pools according to the reasons the costs are assumed to be incurred. |

| | D) | allocate costs to products from pools where costs are accumulated based upon the activities that cause the costs to be incurred. |

|

|

|

| 5 | |

What components are included in voluntary costs? |

| | A) | Prevention and failure. |

| | B) | Prevention and appraisal |

| | C) | Failure and appraisal. |

| | D) | Internal and external failure. |

|

|

|

| 6 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862057/ch5_6_7_8_9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862057/ch5_6_7_8_9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a>

Which of the following is considered to be a direct cost? |

| | A) | Machine maintenance |

| | B) | Machine utilities |

| | C) | Quality control |

| | D) | Wages of production workers |

|

|

|

| 7 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862057/ch5_6_7_8_9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a> Which of the following is considered to be a unit-level cost? |

| | A) | Machine set-ups |

| | B) | Machine maintenance |

| | C) | Material handling |

| | D) | Product engineering |

|

|

|

| 8 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862057/ch5_6_7_8_9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a> Which of the following is considered to be a product-level cost? |

| | A) | Machine maintenance |

| | B) | Rent of manufacturing space |

| | C) | Material handling |

| | D) | Product engineering |

|

|

|

| 9 | |

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862057/ch5_6_7_8_9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (28.0K)</a> If batch-level costs were allocated based upon machine set-ups, how much would be allocated to jeans? |

| | A) | $ 700,000 |

| | B) | $1,050,000 |

| | C) | $1,230,000 |

| | D) | $1,750,000 |

|

|

|

| 10 | |

Which is the following is a difference between activity-based costing and traditional cost allocation? |

| | A) | Activity-based costing utilizes one-step and traditional cost allocation utilizes two-steps. |

| | B) | Activity-based costing utilizes two-steps and traditional cost allocation utilizes one-step. |

| | C) | Activity-based costing utilizes a cost allocation scheme that is based upon a departmental structure and traditional cost allocation utilizes a cost allocation scheme that is based upon activities. |

| | D) | Activity-based costing utilizes a cost allocation scheme that is based upon activities and traditional cost allocation utilizes a cost allocation scheme that is based upon a departmental structure. |

|

|

|

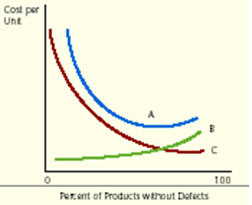

| 11 | |

Line "A" below depicts:  <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862057/ch5_11.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (7.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862057/ch5_11.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (7.0K)</a>

|

| | A) | total quality costs. |

| | B) | total profit. |

| | C) | total quality failure costs. |

| | D) | maximum quality. |

|

|

|

| 12 | |

Tyler wishes to produce 100% of their products 100% defect free. Which of the following statements is true? |

| | A) | Tyler should produce where total quality costs = total failure costs. |

| | B) | A more realistic assumption would be to minimize total quality costs. |

| | C) | Tyler should produce fewer products |

| | D) | Failure cost savings will pay for whatever it takes to reach Tyler's goal. |

|

|

|

| 13 | |

Total quality management: |

| | A) | means managing to minimize total costs. |

| | B) | means managing to achieve high levels of customer satisfaction. |

| | C) | means managing to minimize high levels of customer satisfaction. |

| | D) | means managing to minimize total costs. |

|

|

|

| 14 | |

Information regarding Durden Soap Manufacturing's overhead costs follows: <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862020/ch5_14.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (16.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862020/ch5_14.JPG','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (16.0K)</a>

Activity measures for the two brands of bar soap follow: <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_1a4.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (11.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_1a4.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (11.0K)</a>

What is the total amount of overhead allocated to fat-free soap if Durden uses ABC costing? |

| | A) | $324 |

| | B) | $4,078 |

| | C) | $6,024 |

| | D) | None of the above |

|

|

|

| 15 | |

Information regarding Durden Soap Manufacturing overhead costs follows: <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_15.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (17.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_15.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (17.0K)</a>

Activity measures for the two brands of bar soap follow: <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_15a.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (10.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0078025656/862043/ch5_15a.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (10.0K)</a>

What is the cost per bar of fat-free soap if Durden uses ABC costing? |

| | A) | $ .84575 Per Bar |

| | B) | $1.8445 Per Bar |

| | C) | $8.46 Per Bar. |

| | D) | $84.60 Per Bar. |

|

|