Origin of the Idea

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0077337727/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0077337727/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 18.1 Phillips Curve | | <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0077337727/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 18.2 Long-Run Vertical Phillips Curve |

| <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0077337727/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 18.1 Phillips Curve |

The original Phillips curve did not show the tradeoff between unemployment and inflation in consumer prices, but rather unemployment and inflation in nominal wages. In 1958, A.W. Phillips, a New Zealand-born economist at the London School of Economics, found the famous tradeoff while examining unemployment and wage data for the United Kingdom from 1861 to 1957.

The Phillips curve we know today comes from the work of Paul Samuelson and Robert Solow in 1960. Samuelson and Solow, using unemployment and consumer price data for the United States, found a similar relationship.

While best known for the Phillips curve, Phillips also invented and built the Phillips Economics Computer. Constructed in his garage and presented to the London School of Economics in 1949, the Phillips Economics Computer used water flows to show how money (spending) flows through the economy to affect national income. One of Phillips' machines can be found in the computer exhibit at the Science Museum in London.

| <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=gif::::/sites/dl/free/0077337727/124310/origins_image.gif','popWin', 'width=70,height=90,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (1.0K)</a> | 18.2 Long-Run Vertical Phillips Curve |

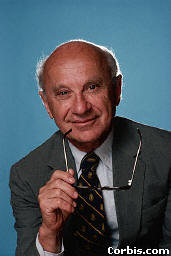

The theory of adaptive expectations comes courtesy of Milton Friedman (b. 1912). Friedman earned his advanced degrees in economics at the University of Chicago and Columbia University, and served on the faculty at Chicago from 1948 to 1977. He is a preeminent economist of the conservative new classical school of economic thought, also known as the Chicago school because of the work of Friedman and others at the University of Chicago. In addition to his work at Chicago, Friedman has worked as a senior research fellow at Stanford University's Hoover Institution, served as president of the American Economic Association in 1967, and won the Nobel Prize in economics in 1976.

Friedman has been a prolific author and speaker, publishing numerous theoretical and popular works in economics. Besides his work on adaptive expectations, Friedman has contributed to our understanding of consumption behavior, crowding-out, and monetary economics.

The theory of adaptive expectations exemplifies Friedman's philosophy that while policymakers might be able to influence the economy in the short run, in the long run the economy will return to its normal state. With that premise, Friedman believes that it is best for the government to play a minimal role in economic affairs.

|  <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0077337727/124320/origin16_2.jpg','popWin', 'width=221,height=326,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (9.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/0077337727/124320/origin16_2.jpg','popWin', 'width=221,height=326,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (9.0K)</a> |

Photograph courtesy of: (c)Roger Ressymeyer/Corbis |