|

| 1 | |

A purely competitive seller's demand curve coincides with all of the following except: |

| | A) | its marginal revenue curve |

| | B) | its average revenue curve |

| | C) | the market price |

| | D) | the industry demand curve |

|

|

|

| 2 | |

Firms in purely competitive markets: |

| | A) | have unit elastic demand curves |

| | B) | are "price takers" |

| | C) | engage in significant advertising |

| | D) | face significant barriers to entry |

|

|

|

| 3 | |

Compared to the downward-sloping demand curve for the output of a competitive industry, a single firm operating in that industry faces: |

| | A) | a perfectly inelastic demand curve |

| | B) | a perfectly elastic demand curve |

| | C) | a unit elastic demand curve |

| | D) | a downward-sloping marginal revenue curve |

|

|

|

| 4 | |

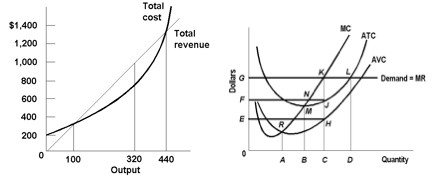

Use the following diagrams to answer the next question.

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/1113273090/384259/quiz21a_4.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (14.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/1113273090/384259/quiz21a_4.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (14.0K)</a>

Refer to the diagrams. Suppose the market price is G, which is the basis for the total revenue curve in the panel on the left. Which output level in the right panel corresponds to an output level of 320 in the left panel? |

| | A) | A |

| | B) | B |

| | C) | C |

| | D) | D |

|

|

|

| 5 | |

Which of the following is a characteristic of equilibrium in long-run competitive markets? |

| | A) | Consumer surplus is minimized |

| | B) | Producer surplus exceeds consumer surplus |

| | C) | Total consumer and producer surplus is maximized |

| | D) | The difference between producer surplus and consumer surplus is maximized |

|

|

|

| 6 | |

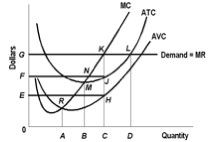

Answer the next question on the basis of the following diagram:

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/1113273090/384259/quiz21a_6.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (7.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/1113273090/384259/quiz21a_6.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (7.0K)</a>

Refer to the diagram. This competitive firm's supply curve connects points: |

| | A) | E and H |

| | B) | G, K, and L |

| | C) | M, J, and L |

| | D) | M, N, and K |

|

|

|

| 7 | |

The market for which of the following most closely approximates pure competition? |

| | A) | feed corn |

| | B) | breakfast cereal |

| | C) | MP3 players |

| | D) | computers |

|

|

|

| 8 | |

The economic profits of firms in long-run competitive equilibrium are: |

| | A) | zero if it is a constant cost industry, positive otherwise |

| | B) | negative |

| | C) | positive |

| | D) | zero |

|

|

|

| 9 | |

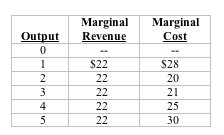

Use the following data to answer the next question.

<a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/1113273090/384259/quiz21a_9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (8.0K)</a> <a onClick="window.open('/olcweb/cgi/pluginpop.cgi?it=jpg::::/sites/dl/free/1113273090/384259/quiz21a_9.jpg','popWin', 'width=NaN,height=NaN,resizable,scrollbars');" href="#"><img valign="absmiddle" height="16" width="16" border="0" src="/olcweb/styles/shared/linkicons/image.gif"> (8.0K)</a>

Refer to the table. Suppose the firm's goal is maximum profits (or minimum losses.) If this firm's minimum average variable cost is $23, the firm will produce: |

| | A) | 0 units |

| | B) | 2 units |

| | C) | 3 units |

| | D) | 4 units |

|

|

|

| 10 | |

An industry comprised of many firms, each of which is engaged in substantial nonprice competition is an example of: |

| | A) | pure competition |

| | B) | monopolistic competition |

| | C) | oligopoly |

| | D) | pure monopoly |

|

|